Revisiting the Dot-Com Bubble and Comparing It With the AI Bubble

The technology can be right while the companies are wrong. That was the expensive lesson of the dot-com bubble.

Contents

When the charts are soaring, you need to see if people are starting to spend more on future stories than on performance.

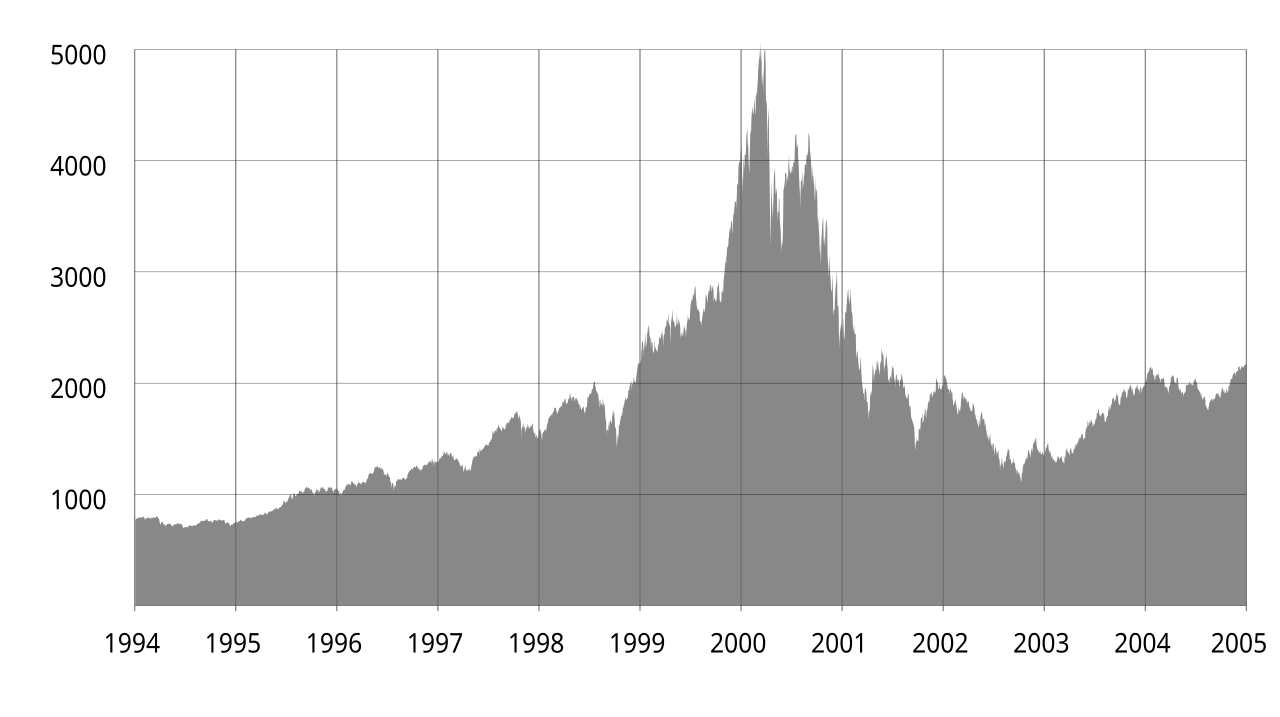

On March 20, 2000, Barron’s ran a brutal warning on its cover. Internet companies were burning through cash too fast. Ten days earlier, the Nasdaq had hit its peak. The market still believed in the “new economy,” but someone had already opened the spreadsheet.

How many months could these companies survive without the next round of funding?

The trigger for the dot-com bubble was not disbelief in the internet. It was money. From mid-1999, the Federal Reserve kept raising rates, and by May 2000 the federal funds rate reached 6.5%. As money became more expensive, the market’s question changed. It stopped asking, “How fast can this grow?” and started asking, “Does this business keep any cash?”

New technology lets strange companies make money

When a new technology arrives, companies with weak foundations can still make money for a while. That is not strange. Early on, nobody knows who the real winners will be. Capital spreads widely because the next Amazon might be somewhere in the pile. The problem is that Pets.com can be in the same pile.

Pets.com was an American online pet-supplies store. It spent heavily on ads, but the business kept losing money, and after the dot-com bubble burst it could not survive. That is why it is still used as shorthand for a weak company that relies on a hot technology trend.

When rates are low, “the next funding round” can start to feel like a business model. Losses look like proof of growth. Advertising spend looks like the cost of winning the market. If stock prices rise and companies can still go public easily, running out of cash feels less like a problem and more like a scheduling issue. Just survive a little longer, and the next check might arrive.

When rates rise, that illusion ends. The next investor disappears. Raising money through a rising stock price stops working. From that point, companies are judged less by their technology story and more by their bank balance. That is how the dot-com bubble broke. The internet was not wrong. The cash math around too many internet companies was wrong.

The Nasdaq overreacted to a technology humanity had never seen before

It is easy to call the Nasdaq foolish in hindsight. But what the market saw then was not entirely wrong. The internet really did change the world. Search, shopping, advertising, news, payments, logistics, social media, and cloud computing were all rebuilt on top of it.

The problem was the timetable. The eventual impact of the technology was huge, but it was far less clear which companies would capture that impact, how much profit they would earn, and when. The market translated “the internet will change the world” into “therefore internet companies can be expensive” far too quickly.

That is the core of a bubble. The technological direction can be right. The price, the company, and the payback period can still be wrong.

AI is facing the same question

AI is now facing a similar question. Whether AI will change the world is not the most important question. It probably will. The real question is this: who earns enough cash, and when, to pay back all this money?

You cannot build data centers with words. You have to buy GPUs, secure power, pay for cooling, and build the facilities first. Corporate AI transformation has a similar shape. The demo looks impressive. People nod in the conference room. Then a few months later the CFO asks:

“How much money did this actually save?”

Companies that cannot answer that question will have a hard time surviving. Some have revenue, but little left after GPU costs. Some have many pilots but weak paid conversion. Some SaaS companies have put in “AI features,” but customers do not want to pay more for them. They look like technology companies, but if rates rise, they look like cash-burning companies.

When a bubble bursts, investors check the actual cash flow first rather than the company's expectations.

This time, the memory is still alive

This is not 2000. Many of the people who lived through that period are still part of the market’s mainstream. Former operators, investors, and founders from that era are now executives, board members, and fund partners. Society has not had enough time to forget the lesson of the dot-com bubble.

So this cycle may not repeat as a line of revenue-less websites rushing into public markets. The overheating may be more hidden in private valuations, long-term leases, GPU rental economics, private credit, and hyperscaler data center contracts. It may show up late on stock charts, even though the money has already been committed.

Memory does not eliminate greed. It changes the shape of the bubble.

Companies that should fail should fail

I do not see it as purely bad when companies that should fail actually fail. If weak companies stay alive too long, they drag the real technology down with them. The internet became larger after the dot-com crash. The survivors proved themselves with cash flow, not advertising spend.

AI may go through the same sorting process. AI can be real. That does not mean every AI company is a real business.

If rates rise again, the market will not only look at model performance. It will ask whether customers pay. It will ask whether anything remains after GPU costs. It will ask how many months a company can survive without the next round. At that point, the AI trade moves from the product demo to the calculator.

In this rate cycle, the question I care about is simple. Not who talks about AI. Who makes money with AI?

Sources

- Barron’s, “Burning Up”, March 20, 2000.

- Federal Reserve, FOMC minutes, May 16, 2000.

- Goldman Sachs, The Late 1990s Dot-Com Bubble Implodes in 2000.

- Bank for International Settlements, Financing the AI boom: from cash flows to debt, January 7, 2026.

- Wikimedia Commons, Nasdaq Composite dot-com bubble.svg, public domain.

{kind=link}